How Foreign Buyers Can Get a Mortgage in Spain (2026): Non-Resident Rules in the Valencia Region and Costa Blanca

Buying a new build property in Spain often raises the same practical question for overseas buyers: is it possible to obtain a mortgage without living in the country?

The answer is yes. Spanish banks regularly lend to international purchasers, particularly in areas with established foreign demand such as the Costa Blanca and the Valencia region. However, mortgages for non-resident buyers follow slightly different rules than those available to Spanish residents.

Loan-to-value ratios are lower, documentation requirements are stricter, and banks will examine income stability carefully. Understanding how the process works in advance makes the purchase significantly smoother.

This guide explains the typical mortgage conditions for foreign buyers in Spain in 2026, how banks assess applications, and what to expect when financing off-plan apartments or new developments in the Valencia region. At the end of the article, you can download a detailed roadmap on how to get a mortgage in Spain.

Key Takeaway: You can get a Mortgage of up to 70% as a Non-Resident of Spain

Foreign buyers can usually obtain a Spanish mortgage covering around 60–70% of a property’s value, meaning purchasers typically need 30–40% of the price in cash plus purchase costs. Mortgages are commonly available for new build property in Spain, particularly in established areas such as Costa Blanca developments and the Valencia region.

What Is a Non-Resident Mortgage in Spain?

A non-resident mortgage in Spain is a property loan issued by a Spanish bank to buyers who do not live or pay taxes in Spain.

These mortgages are designed for international purchasers who wish to buy a home in Spain while remaining resident in another country, such as the UK, the United States or another EU state.

Compared with mortgages for Spanish residents, the key differences are:

Despite these differences, the structure of the loan is otherwise similar. Mortgages are issued in euros, secured against the property itself, and repaid through monthly instalments over a fixed term.

Mortgage Support for Overseas Buyers

Spaces & Places Exclusive Property S.L. works with several Spanish banks active in the Valencia region and Costa Blanca.

Our team holds the Informador en Crédito Inmobiliario (ICI) certification, a qualification required in Spain for professionals who provide information about mortgage products under the Spanish Mortgage Law.

This allows us to:

Mortgage approval always depends on the bank’s final assessment of the borrower’s financial situation.

Mortgage Snapshot: Spain 2026

While conditions vary slightly between banks, the overall framework tends to be similar across Spain.

Factor | Typical Conditions |

|---|---|

Loan-to-value | 60–70% of property value |

Mortgage term | Up to 30 years |

Maximum age at maturity | Usually 70–75 |

Interest rates | ~2.6% – 3.7% depending on products |

Deposit required | 30–40% of purchase price |

Approval timeframe | 2–4 weeks after documents submitted |

Typical Interest Rates in Spain (2026)

Spanish mortgage rates remain relatively competitive compared with several other European markets.

In early 2026, foreign buyers typically see offers within the following ranges:

Fixed-rate mortgages

approximately 2.8% – 3.7%

Reduced rates with bank products

approximately 2.55% – 2.9%

Spanish banks often offer lower rates if the borrower agrees to additional financial products, sometimes called bonificaciones. These may include:

Buyers are not obliged to accept these products, although declining them usually results in a higher interest rate.

How Much Deposit Is Required?

Because banks usually finance no more than 70% of the purchase price for non-residents, buyers should expect to provide the remaining funds themselves.

A typical purchase structure looks like this:

Purchase costs normally include:

Example Purchase

For a €350,000 new build townhouse next to Valencia:

Item | Approximate Amount |

|---|---|

Deposit (30%) | €105,000 |

Purchase costs (10–12%) | €35,000–€42,000 |

Total funds required | €140,000–€147,000 |

We discuss in more detail what the final cost of purchasing a new home in Spain consists of in this article.

What Documents Do Spanish Banks Require?

When applying for a mortgage in Spain as a non-resident, banks focus primarily on income stability, existing financial obligations and the buyer’s overall financial profile.

The goal of the documentation process is straightforward: the lender needs to confirm that the borrower can comfortably manage the mortgage payments over the long term.

In practice, most Spanish banks request a similar set of documents from international buyers. While requirements vary slightly between lenders, the following are typically needed.

What you should prepare for the bank:

Spanish lenders examine both the borrower’s finances and the property itself.

Most non-resident buyers will need to provide:

Personal documentation

Financial documentation

For self-employed applicants, banks usually request:

The goal is to confirm stable income and manageable debt levels.

A useful rule of thumb: if something matters to you — sea view line, parking space, terrace size, fixtures — it needs to appear in the written pack, not just in a brochure or a video call.

How Spanish Banks Assess Affordability

When reviewing a mortgage application from a foreign buyer, Spanish banks focus primarily on whether the loan will remain comfortably manageable over time.

As a general guideline, lenders prefer that the monthly mortgage payment does not exceed roughly 30–35% of the borrower’s net household income. This threshold helps ensure that the loan remains sustainable even if financial circumstances change.

In addition to income, banks typically review several other aspects of the applicant’s financial situation, including:

For buyers whose income is paid in a non-euro currency, some lenders may apply additional internal risk assessments to account for potential exchange-rate fluctuations.

Because of this, applicants with stable income, moderate debt levels and clear financial documentation generally find the mortgage approval process smoother.

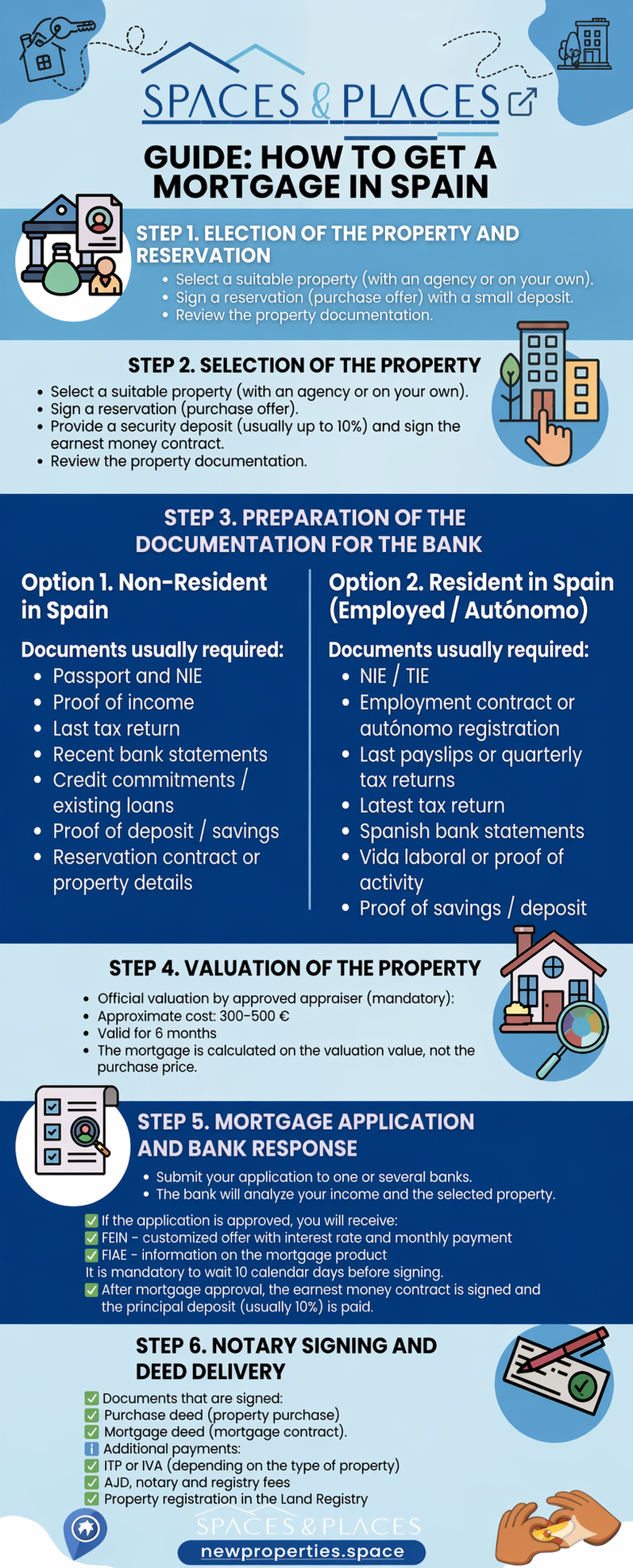

The Mortgage Process When Buying a New Build Property

The mortgage process usually runs alongside the property purchase itself. For off-plan developments, the mortgage is typically formalised when construction is completed.

The sequence generally follows six steps.

1. Choosing the Property

The buyer selects a home and signs a reservation agreement, usually paying a small reservation deposit.

2. Signing the Private Purchase Contract

A private purchase agreement is signed, and the buyer pays an initial deposit — commonly around 10% of the purchase price.

3. Preparing Documents for the Bank

Financial documents are submitted to one or more banks for analysis.

4. Property Valuation (Tasación)

An independent surveyor carries out an official valuation.

Typical valuation cost:

€300–€500

The mortgage amount is calculated based on the valuation value, not necessarily the purchase price.

5. Mortgage Approval

If approved, the bank issues two mandatory documents under Spanish mortgage law:

• FEIN — the binding mortgage offer

• FIAE — the mortgage information document

Borrowers must receive these at least 10 days before signing.

6. Completion at the Notary

At completion, two deeds are signed:

• the property purchase deed

• the mortgage deed

Both are signed before a Spanish notary, after which the property is registered in the Land Registry.

Expert Insight from Spaces & Places

In our experience assisting international buyers purchasing new developments in the Valencia region, mortgage approval often depends less on nationality and more on clear financial documentation and stable income history.

Preparing documentation early – particularly tax returns and proof of income – tends to shorten the mortgage approval process significantly.

Mortgage Costs Buyers Should Consider

Besides the deposit and taxes, buyers should also account for several mortgage-related expenses.

These may include:

Under recent Spanish legislation, many administrative mortgage costs are now paid by the bank, which has reduced upfront expenses for borrowers.

Infographic: A Visual Overview of the Mortgage Process

The mortgage process in Spain follows a fairly structured sequence, from choosing the property to signing the final mortgage deed.

The infographic below summarises these steps and the documentation typically required during a Spanish mortgage application.

{kind=link}

Spain’s New Build & Mortgage: Approval Risk at Completion

One point that deserves careful attention when buying an off-plan property in Spain is timing.

The mortgage is not agreed at reservation stage, but only when the property is completed and ready for signing.

In practical terms, this means buyers are committing a substantial deposit (often 20–30%) before any final lending decision is made. Spanish banks will reassess your profile at completion, using updated income, debts and interest rate conditions at that moment. A change in employment, exchange rates or lending criteria can affect the outcome.

For buyers of new build property in Spain, this is less about uncertainty and more about planning ahead. It is sensible to approach a purchase with a clear view of borrowing capacity, allowing for a margin of safety rather than relying on maximum lending assumptionsIn practice, buyers often compare this route with independent mortgage offers, sometimes with guidance from local agents familiar with new build property in Spain and the lending criteria applied to international clients.

So buying off-plan apartments in Spain involves a two-step commitment: first your own funds, and only later the bank’s. Understanding this structure early helps avoid surprises and supports a more confident purchase process, especially if you plan to start purchase process remotely.

A Practical Perspective

Buying a new build property in Spain, particularly off-plan, involves more than choosing the right development. Payment schedules, mortgage approval at completion, and the way Spanish banks assess non-resident buyers can all influence the outcome.

At Spaces & Places Exclusive Property S.L., we work with international buyers across the Costa Blanca and Valencia region, and see these questions come up consistently, especially around financing at completion and how different mortgage routes compare in practice.

In many cases, the difference is not access to a mortgage, but understanding how the process works before committing to an off-plan purchase.

FAQ: Mortgages for Foreign Buyers in Spain

About the author

SPACES & PLACES Exclusive Property S.L.

Information in this article is intended for general guidance only. Development details, pricing and availability may change; please verify all information directly with the developer or your trusted adviser before making any purchase decisions.

New Project in Denia, Spain

Talasa Caelus brings sustainable seaside living near Dénia: elegant new-build homes with spacious terraces, landscaped gardens and pools, blending design, comfort and energy efficiency.

Key-Ready Townhouse in Valencia Suburbs

Modern turnkey home with private garden, terrace and high-quality finishes; featuring bright interiors, energy-efficient design and ready for immediate move-in.

New Penthouse in Valencia

Exclusive new-build penthouses in Cabanyal, Valencia. 3 bedrooms, terraces and eco-friendly design close to the sea and city centre.